You don’t need to be rich to invest. It’s for everyone no matter their age, and it’s one of the most effective ways to build long-term wealth. Investing may seem overwhelming and you’re probably wondering where to begin. Well, here we go!

What is investing?

Investing is the act of putting money into something that will give you an expected return in the future. This can be done for many reasons including profit, growth, or simply saving for retirement.

Investopedia defines investing as ‘the act of allocating resources, usually money, with the expectation of generating an income or profit.’

Buying stocks is one of the easiest ways for new investors to get their feet wet when investing. However, investing also comes with the risk of losing money.

How does the stock market actually work?

When you invest in a stock, you’re buying a small piece of ownership in a company known as a “share.” As a part-owner, you’ll get a cut of the profits if the company grows and earns money. However, your investment is also at risk if the company struggles due to recession, losses, or even complete failure.

Individual stock prices rise and fall depending on their perception among investors, who base their perceptions on factors ranging from global economic conditions to corporate actions to simple supply and demand.

As well as earning profits in the form of possible dividends, you can also earn money through appreciation where the value of the stock you own increases over time due to increased demand, company growth, or all sorts of other market factors. Remember that the value of a company can fall for exactly the same reasons.

Whilst stocks are usually the most common asset within an investment portfolio, they are by no means the only type of security (exchangeable, tradable financial assets such as a stock, bond, or option) or asset you can purchase.

Investing vs saving – why investing may be worth the risk

If you’re considering investing some of your hard-earned cash you might ask yourself why you would choose something risky instead of putting it away for safekeeping. Whilst investment involves some risks, there’s an equally strong case for saying that not investing may be even riskier.

Because…. inflation.

Let’s say that back in 2010, you took a one-dollar note and put it in a piggy bank. Today, that same note wouldn’t have the same value because the cost of everything has increased. Ever heard someone moan about how cheap food used to be? This is because inflation reduces the value of money, year after year.

Let us imagine that you took that same dollar and put it into an interest-earning savings account instead. With the average savings account earning a moderate interest of about 0.1% annual percentage yield (APY) that dollar would be worth $1.01 today. It still wouldn’t keep pace with the 17% inflation rate, but you would be slightly better off than doing nothing

Now, imagine you invested that dollar in the stock market instead… Although your exact results would vary depending on what you invested in, the average annual return on stock market investments over the last decade (according to the S&P 500 index which tracks 500 of the largest publicly traded companies) is about 10%. So that single 2010 dollar would now be worth $2.46 which definitely keeps pace with the rate of inflation including a nice profit.

From these simple examples you’ll see that by investing, you’ll be able to better combat inflation, increasing the chances of being able to buy the same amount of stuff in the future that you can now.

It’s important to note that these investments should not include your emergency savings account. Common wisdom suggests allocating three to twelve months of take-home pay to savings for emergencies.

It’s all about finding the right balance and assessing your personal goals.

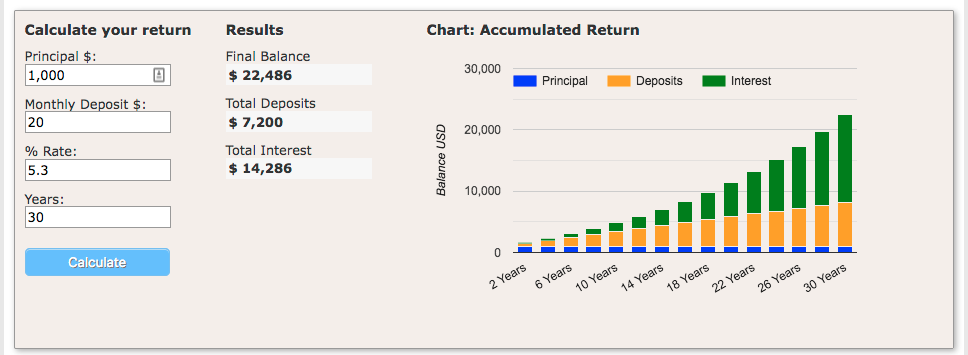

Investing early lets you take advantage of compound interest

It’s easy to put off investing for another time, especially with bills and other responsibilities fighting for your hard-earned cash. But the earlier you start investing, the more benefit you gain from compounding.

Compound interest is essentially a snowball effect where you start earning money on the money your investments have already earned. Basically, you are increasing your earnings just by staying invested in the market longer.

It is much more manageable to invest a regular smaller amount when you are younger than waiting and having to invest five or six times as much when you are older.

Time can also protect you against risk. Taking financial risks when you’re young can result in big wins and the younger you are, the more time you have to rebuild after any losses. Have a look at this graph that illustrates the difference between compound and normal interest.

Source: http://www.helpfulcalculators.com/compound-interest-calculator

Figuring out what kind of investment is right for you

Risk tolerance and diversification

All investments have some level of risk because the market is volatile – it moves up and down over time – which can make some people very uncomfortable when markets decline. To help choose which approach is best for you it’s important to understand your personal risk tolerance and how much volatility you can handle.

A good rule to stick to as a new investor is to diversify and make sure to spread your capital across various different investment types so you reduce your investment risk. For example mutual funds and exchange-traded funds allow investors to purchase baskets of securities instead of individual stocks and bonds.

Financial goals

Because investments have such strong long-term growth potential, many people use them as savings vehicles for major, future financial goals, like purchasing a home or retirement. Figuring out which strategy is right for you begins by assessing and understanding what you want to achieve.

Establishing clear short and long-term saving and investing goals will help you develop a solid plan.

Your time horizon

Patience is key when investing and long-term investments tend to yield higher returns. That’s because investments need time to grow and need time to adjust to the ups and downs of the market.

Most people invest with their retirement in mind because retirement is expensive. Investing early is a smart way to reduce your chances of running out of money after you retire.

On any day, the stock market can plunge and economies can take an extended downturn. If you give in to fears caused by market fluctuation and sell stocks during a market dip, you stand to lose quite a bit of your investment. Over time, investors who are in for the long run are more likely to come out ahead.

Active or passive

You’ll also need to decide whether you’d like to be an active investor or a passive one. Passive investors typically own assets like diversified funds that charge low fees, whereas active investors might choose individual investments or funds that aim to outperform the market. Many studies have shown that, over time, passive investing tends to outperform active investing.

Do-it-yourself or use an advisor?

You can also choose between managing your own investments through an internet broker or hiring a financial advisor (or a robo-advisor). You’ll likely incur fewer costs if you do it on your own, but an advisor can help you if you’re just starting out.

Taxes

Don’t forget that if you own investments in an individual or joint account, you’ll most probably need to pay taxes on any interest, dividends, and capital gains you earn. You can avoid these tax penalties by owning investments in tax-advantaged retirement accounts such as Individual Retirement Accounts (IRAs).

How much money do I need to start investing?

Good news – you don’t need as much money as you’d think to start investing.

Most online brokers have no account minimums to get started and some offer fractional share investing for those starting with small amounts. In fact, you can purchase Exchange Traded Funds (ETFs) for just a few dollars to allow you to build a diversified portfolio of stocks.

Micro-investing sites will even let you round up your purchases made through a debit or credit card as a way to start investing.

First set a budget

How much you are able to put towards your investments can help you decide a lot of other parts of your investment strategy like where to open your account and what securities to invest in.

The first steps in working out how much you can regularly contribute:

- thoroughly understand your expenses

- be clear and realistic about what you are trying to accomplish

- don’t worry about starting out small

- pay off any high-interest debt before investing large sums of money

Asset allocation – how much to invest in stocks

IMPORTANT TO NOTE: The stock market may not be the right place to put money that you might need within the next five years, at a minimum. This is because while the stock market will almost certainly rise over the long run, there’s simply too much uncertainty in stock prices in the short term – it is not unusual for drops of up to 20% in a given year.

Deciding what to do with your investable money (money you aren’t likely to need within the next five years) is known as asset allocation. A few factors are crucial here like your age, risk tolerance and investment objectives.

If you’re young, you have decades ahead of you to ride out any ups and downs in the market, but this isn’t the case if you’re retired and reliant on your investment income. Hence, as you get older, stocks may become a less preferable choice.

For years, this rule of thumb has helped simplify asset allocation: individuals should hold a percentage of stocks equal to 100 minus their age. So, for a typical 60-year-old, 40% of your portfolio should be in stock-based funds with the remainder in fixed-income investments like bonds or high-yield Certificate of Deposits (High Yield CDs.)

From this starting point, you can adjust the ratio up or down depending on your specific risk tolerance. If you’re more of a risk-taker or are planning to work past the typical retirement age, you may want to increase the ratio of stocks. If you don’t like big fluctuations in your portfolio, you might want to modify it the other way.

Basic types of investments

These are the foundation of any investment strategy. You could invest in all sorts of things, but most would fit into just a few broad categories called “Asset Classes.”

The most popular asset classes are:

- Equities/Stocks

- Fixed Income investments/Bonds

- Cash and cash equivalents like money market funds

Alternative asset classes are:

- Commodities and futures, such as oil and gold

- Investments like real estate, foreign exchange (forex), and collectibles like fine art

- Sustainable, Responsible, and Impactful investments (SRI) focussed on beneficial social or environmental impact

Alternative investment tends to be less liquid than conventional assets. For example, stocks are highly liquid assets but a private equity investment requires tying up your investment capital at least for 5–7 years.

Sometimes it’s best to invest your money in productive assets, which generate income from some sort of activity. For example, if you buy a piece of art, years from now, you’ll still own only the piece, which may or may not be worth more money. But if you buy an investment property, in 40 years you’ll not only have the building, whose value may have gone up; you’ll also have earned 40 years of rental income.

Each type of productive asset has its own benefits, risks, and tax rules but the most common for new investors are stocks and bonds.

Stock or equity investing

If you hear the word “invest” you’ll probably think of equity investments immediately. It entails the buying and selling of stocks in companies that are traded publicly. It is a popular investment for beginners as they have often offered the best long-term returns. But they could also be talking about buying partial ownership of a private company.

Investing in privately-held companies

Investing in publicly traded companies

Private businesses can sell pieces of ownership of the company known as “shares or stocks” in a process known as an initial public offering or IPO. By selling shares, companies are able to raise capital to help them grow or expand. Once a business has become public and its shares are traded on an exchange, anyone who buys the stock can become a partial owner.

Stock investors may buy stocks for the following reasons:

- profit from increases in a stock’s price

- sell stocks to profit from a decrease in the stock’s price

- buy or sell options on stocks or stock indexes

- profit from receiving stock dividends on stocks they own (like earning interest or a per-share bonus)

- to have a say in electing the board of directors

Stocks are traded on exchanges such as the London Stock Exchange (LSE) or the New York Stock Exchange (NYSE) who regulate and facilitate the exchange of ownership.

The factors determining the price of a stock are:

- how well the company is performing

- how well the overall industry the company is part of is performing

- the performance of competitors

- economic conditions

- government actions

People often ask or get confused with bull and bear markets. Here’s an easy way to remember which is which:Bull markets: Think of an actual bull. It charges and is volatile. So bull markets often charge i.e. the value goes up very quickly. But bulls also stop at some point, and the markets drop. During bull markets investors are confident and eager to buy stocks. Bear markets: A bear is much more placid. They hibernate in winter but wake up in summer. Like bears, bear markets can go into a slumbering mode where there is not much activity. They wake up at times and show sharp increases that last longer. In bear markets investors are nervous and want to sell their stocks because they are afraid that the market will crash.

Your risk tolerance and where you are in your life will determine what kind of investments you make. If you are comfortable with stability, blue-chip stocks are more suitable for you because they have an established track record of earnings and stakeholder dividends.

Other people like a certain amount of risk. You might win more on upswings but remember you’ll also lose more when markets are down. You should have a look at buying growth stocks in bull markets. Growth stocks can be volatile. They tend to show bigger gains in bull markets and they drop faster in bear markets.

You might be someone that knows your way around stock markets. And this is not your first rodeo. In that case you’ll be on the lookout for bargains in undervalued companies or value stocks. A challenge you might face is to keep track of all your stocks and potential companies you’re interested in. Have a look at https://app.exirio.com/. Download the app and track your wealth, all in one place.

A bit more about stocks. Stocks can be quite risky. Everybody wants to pick the next Amazon. But not all stocks are created equal. In the investment universe you can count yourself extremely lucky if you picked a stock like Amazon that has gained value and grown beyond expectations. Putting all your eggs in one basket or one stock is not a good idea. If that stock fails, you’ll lose all your hard-earned money. Most investment advisors – and common sense – will tell you to diversify and invest in various stocks, markets, and asset classes.

Fixed income investments or bonds

Bonds are investments in debt securities that yield a fixed-rate interest payment over a period. Otherwise known as the life of the bond, or debt security. The bond market is one of the biggest markets in the world because most governments carry massive amounts of debt. The money you spend on buying a bond basically goes towards financing a government or company. In return you’ll receive a specified interest rate, otherwise known as a coupon rate. You’ll typically receive the interest you’ve made annually or semi-annually until you’ve received the full principal amount of the bond back on the maturity date.

Interest rates fluctuate over the lifetime of the bond. That means the value of the bond and its yield until maturity change. The coupon rates stay the same but as interest rates change the value and yield of the bond reflect those changes. So, when interest rates rise bond prices will fall. As interest rates fall bonds increase in value. If you hold a bond until its maturity date these fluctuations will not affect you. Your yield will change only when you buy or sell a bond before the maturity date.

Bonds are very popular because they carry relatively low risk, if you invest in a country like the UK or USA.

You can trade bonds like you would trade stocks or shares. US Treasury bonds are considered rather safe because investors know that the federal government will meet their obligations. Another bond to consider is municipal bonds issued by cities, towns, state governments or countries. They are exempt from federal income taxes and in some cases state and local taxes as well.

Corporate bonds depend on the perceived creditworthiness of the company. Companies that are vulnerable to credit or carry a default risk are called high-yield or junk bonds.

Bonds are sensitive to interest rate hikes. The yield you receive on a bond is based on the interest, or coupon, rate. Same as for government bonds, when yields go up, corporate bond prices go down. And when prices go up, yields come down.

Bonds offer a valuable and predictable growth to your portfolio, but they will not make you rich, nor will they fund a comfortable retirement on their own. As we said earlier. Diversity’s the word.

Zero-coupon bonds

Another type of bond is a zero-coupon bond. These bonds do not pay periodic coupons, but they are sold at a discount to their face value, to compensate for the lack of cash flows during the life of the bond.

Bond sellers

State, national and municipal governments sell bonds. Investors are very attracted to municipal bonds because they often do not carry tax on interest. You can also buy corporate bonds that deliver higher yields, but they also carry higher risk.

In recent years bonds, whose value depends on interest rates and credit worthiness of the issuer, have not seen a huge amount of success among small investors at least, as we have gone through a period of record-low interest rates. This has translated into meager coupon returns, some say (more often than not) too low when compared to the risk assumed with the investment.

Where will you hold these investments?

Now that you know what assets want to buy, you must choose where to hold them. You can open a taxable brokerage account that’s not connected to a retirement account. If your employer offers a 401(k) plan you can invest through them or you can invest in one of the various individual retirement accounts (IRAs) on offer. Here are some options of IRAs:

- Traditional – for individuals

- Roth – for individuals

- Simple – for employees and owners of small companies

- SEP-IRA – for employees and owners of small companies

Something to keep in mind when you choose between all the options. Do you want to invest tax-free dollars and pay taxes on your gains (a traditional IRA) or do you want to invest after tax money and pay no taxes on your yields (a Roth IRA)? If you want to look at the 401(k) plan, have a look and see if your employer will match your contributions? It really makes quite a difference.

If you invest in real estate, you might want to keep your holdings in a limited liability company (LLC) or limited liability partnership (LLP). Speak to a legal or accounting professional to help you choose and set up the relevant structures.

Different ways to invest your money

High-yield savings accounts

A high-yield savings account is a type of savings account that typically pays up to 25 times the national average of a standard savings account.

In the past this was as simple as a savings account at the same bank where you hold your checking account, making transfers between the two easy and quick. But now that online banking and internet-only banks have increased competition there are many options to choose from.

Carefully compare high-yield savings account options by comparing factors such as initial deposit requirements, interest rates, minimum balance requirements, and any possible account fees.

Certificates of deposit (CDs)

A certificate of deposit (CD) is a savings account that provides an interest rate premium in exchange for you agreeing to leave a lump-sum deposit untouched for a set amount of time eg. six months, one year, or five years. When you cash in or redeem your CD, you receive the money you originally invested plus any agreed-upon interest.

Almost every bank, credit union, and brokerage firm will offer a range of CD options with returns typically three to five times higher than the industry average for every term, so it definitely pays to shop around.

Employer retirement plans

If you have a retirement plan at work, it’s probably the first place you should put your money, especially if your company matches a portion of your contributions. That match is free money and a guaranteed return on your investment.

If you’re on a tight budget, try to invest just 1% of your salary into the retirement plan. You probably won’t even miss a contribution that small. Then when you’re comfortable with that you can increase it as you get annual pay increases.

Individual stocks

Is it worth the time and risk to have single stocks in your portfolio? Having single stocks in your portfolio can reduce fees, help you to understand the tax implications, and allow you to get to know the companies you own better. But they need you to invest more time managing your portfolio and can increase your risk through a lack of diversification.

Index funds

An index fund is a type of mutual fund or exchange-traded fund (ETF) with a portfolio constructed to match or track the components of a financial market index, such as the Standard & Poor’s 500 Index (S&P 500).

Index funds are popular with investors because they promise ownership of a wide variety of stocks, greater diversification and lower risk – usually all at a low cost. That’s why many investors, especially beginners, find index funds to be superior investments to individual stocks.

Target date mutual funds

Target retirement funds are designed to be the only investment vehicle that an investor uses to save for retirement. Also referred to as life-cycle funds or age-based funds, the concept is simple: Pick a fund, put as much as you can into the fund, then forget about it until you reach retirement age.

Of course, nothing is ever as simple as it seems. While simplicity is one of the pros of these funds, investors still need to stay on top of fees, asset allocation, and the potential risks.

Mutual load funds

A load fund is a mutual fund that comes with a sales charge or commission. The fund investor pays the load, which goes to compensate a sales intermediary, such as a broker, financial planner, or investment advisor, for his time and expertise in selecting an appropriate fund for the investor. The load is either paid upfront at the time of purchase (front-end load), when the shares are sold (back-end load), or as long as the fund is held by the investor (level-load)

Exchange-traded funds (ETFs)

An exchange-traded fund (ETF) is a basket of securities that trade on an exchange just like any other stocks. They can contain a combination of all types of investments like stocks, commodities, or bonds and can be structured to track anything from the price of an individual commodity to a large and diverse collection of securities

ETFs are different from mutual funds in that their share prices fluctuate all day rather than once a day after the market closes and they usually offer lower expense ratios and fewer broker commissions than individually buying the stocks.

Robo-advisors

A robo-advisor is an investment management service that uses algorithms to build and look after your financial portfolio using computer models to determine the best portfolio mix for your unique needs based on your age, income and goals.

When you open a robo-managed account you supply basic information about your investment goals online. Robo-advisors will then build your portfolio from mostly low-cost ETFs and index funds – groups of investments that often reflect the behavior of the S&P 500 or another index.

Using a robo-advisor can be a good move for beginner investors because they allow you to quickly manage your investments without consulting a financial advisor. They also tend to have low account minimums and low management fees. However, you’ll pay the fees charged by index funds and ETFs, called expense ratios, in addition to that management fee.

Micro-investment apps

Micro-investing apps, such as Acorns or Stash, are types of robo-advisors that allow you to save and invest money in really small amounts.

By linking a credit or debit card, these apps round up purchases to the nearest dollar. When you reach a certain amount in spare change, the app invests that money for you into a diversified portfolio. You can also opt to have a specific amount of money transferred from your bank account to the micro-investing app each week.

Like robo-advisors, these apps invest your funds into a portfolio of ETFs which means that your investments are then diversified across thousands of stocks and bonds. Some also let you choose a portfolio based on your risk tolerance.

While micro-investment apps are easy to use, returns are minimal so some experts suggest saving your spare change elsewhere.

Annuities

Annuities aren’t technically investment products – they’re a type of insurance policy issued by financial institutions with the intention of paying out invested funds in a fixed income stream in the future. In times of market uncertainty, they are popular as they can provide added security in retirement planning.

The accumulation phase is the first stage where investors fund the product with either a lump-sum or periodic payments. After the annuitization period, the annuitant receives payments for a fixed period or for the rest of their life.

Annuities are highly customizable, can be categorized into immediate and deferred annuities and are structured in the following ways:

- fixed annuities – provide a stable payout

- variable annuities – fluctuate based on market changes

As for any investment product, the devil is in detail. You need to thoroughly understand the fees implied and be comfortable with the underlying investment strategy of the product you are buying.

Investment tax basics

Taxes are due when you sell an investment or stock for a profit. Other taxes are raised when you receive a dividend. Because taxes vary from country to country it makes sense to consult a tax specialist to help you navigate the complicated landscape of tax and investments. Here are some basics to look out for.

Capital gains tax

You don’t pay tax on the investment amount that you spent on your stocks. Tax is charged only on the profit portion of your stock. This applies to other investments like art and property as well. When you buy something at a price and sell it later at a higher price, it’s known as capital gains and it’s taxable depending on the tax laws in your country. Governments tend to look at capital gains gathered over a longer period more favorably than short-term gains.

Capital losses

When you sell an investment for less than what you paid for it you’ve made a loss. One of the few advantages of making a capital loss is that you can deduct it from your capital gains. For example: you sell one stock for a profit of $3,000 and another at a loss of 2,000. You will only be charged on the net capital gains of $1,000.

Taxes on dividends

Dividends are paid by companies to their shareholders or holders of their stock. There are two kinds of dividends namely qualified and unqualified. Unqualified dividends are also known as ordinary dividends because they are taxed as ordinary income. Qualified dividends normally carry a lower tax rate, and must meet the following criteria.

- Must be paid by a qualified corporation or foreign entity

- You must own it for a certain amount of time

People in higher tax brackets generally pay higher taxes on dividends than lower income groups. To alleviate your tax burden you can choose to hold your foreign stocks and taxable bond mutual funds in a tax-deferred retirement account like a 401(k) plan or an IRA.

How to invest

All the advice and knowledge is useless if you don’t have a way to actually buy stocks. You need a specialized type of account to trade stocks called a brokerage account. It is a simple process to open a brokerage account. You just need to find a company that offers this kind of service, do an EFT or wire transfer or mail a check. There’s a couple of things to consider when you choose a broker.

Brokers

A broker is an intermediary between an investor and a securities exchange. Because securities exchanges only allow orders to be placed by exchange members (Brokers), investors require their services to place their orders. Brokers are compensated in various ways, either through commissions, fees or they are paid by the exchange itself.

An online broker is a broker that deals with customers over the Internet instead of by phone or in a physical office. Online trading is convenient – you can place orders, check quotes and make changes from anywhere – and facilitates much faster execution of trades. It also comes with lower costs than an advisory service. There are many options out there depending on your investment experience and goals so do your research to get the most for your money.

Type of account

You need to decide what kind of account you will need. For investors who want to learn stock market investing there’s the option of a standard brokerage account or an individual retirement account. Both of these will enable you to buy stocks, ETFs and mutual funds. You need to remember why you’re investing in stocks and how quickly you can access your money when you want to. You’ll need a standard brokerage account if you want to access your money easily, are investing as a backup safety net or if you want to invest more than the IRA contribution limit that is applied annually.

If your goal is to build a comfortable retirement for yourself an IRA will make more sense. You can choose between two different types of IRA accounts. Traditional and Roth IRAs. There are also specialized types of IRAs aimed at people who are self-employed or business owners, they include SEP and SIMPLE IRAs. IRAs offer great tax benefits but it can be difficult to access your money in a hurry.

Compare costs and features

Most online stock brokers charge more or less the same but they offer various other benefits. Some brokers offer educational tools, analysis and research that can be very useful especially for novice investors. Other brokers open the door for you to trade on foreign trade exchanges. Although online stock trading is very convenient you might want to speak to a broker face-to-face for guidance. Some brokers do have physical offices that will accommodate you. Something else to think about is how user-friendly the broker’s trading platform is. Some are much more clunky than others. Try the demo version of various sites before you go all in with your money.

Commissions and Fees

Nobody works for free. Brokers are no different. They charge a commission every time you buy or sell a stock. These fees vary and depend on the size of the transaction you do. Although the fees might seem small it all adds up if you buy and sell often. Keep this in mind. If you hop in and out of positions frequently these fees can become more than the actual profit you might be making.

A trade is when you buy or sell shares in one company. If you trade in five different companies or stocks, it is seen as five trades and it will be charged accordingly. Take the $1,000 profit we mentioned earlier. If you trade in five companies you’ll pay $50 in trading costs (if the fee is $10 per trade). So you’ve already lost 5% of your investment before your stock has had time to grow.

Welcome to the exciting world of investing and trading in stocks. Keep an eye on how your stocks are doing but don’t react impulsively every time there is a rise or slump in the market. Consider your position, look at the general economy and make your decisions based on facts not emotions.

Happy trading.

Try our demo or register a new account